FBAR Please Help

Jul 2nd 2025 | 9:31 am

Jul 2nd 2025 | 9:31 am

#1

Thread Starter

Forum Regular

Joined: Jun 2020

Posts: 96

Hi all,

I just found out about FBAR and FATCA. I contacted a lawyer and he wants to charge me an astronomical $28k for filing forms for past violations that I had no clue about since I got my greencard some years ago.

I work in the USA as a permanent resident.

What can I do? I file tax every year in the USA but no one told me about this stuff.

Surely they cannot charge me just because I had some funds in my UK bank. This is crazy and feels like a total scam.

Please advise.

Ed

I just found out about FBAR and FATCA. I contacted a lawyer and he wants to charge me an astronomical $28k for filing forms for past violations that I had no clue about since I got my greencard some years ago.

I work in the USA as a permanent resident.

What can I do? I file tax every year in the USA but no one told me about this stuff.

Surely they cannot charge me just because I had some funds in my UK bank. This is crazy and feels like a total scam.

Please advise.

Ed

Jul 2nd 2025 | 10:47 am

#2

Forum Regular

Joined: Oct 2021

Posts: 76

DO NOT PAY THIS LAWYER ANYTHING TO FILE YOUR FBAR ETC.!! I was in a similar situation, our accountant in NY wanted to charge me $10,000 to file FBAR’s, I did it myself online, it’s a little time consuming but it’s relatively simple. The IRS are not going after you to extract back taxes from you or to penalise you, it’s more about money laundering. They realise that most people aren’t aware of this so are pretty lenient & understanding.

Jul 2nd 2025 | 10:58 am

#3

Thread Starter

Forum Regular

Joined: Jun 2020

Posts: 96

Thank you for your reply, which is somewhat reassuring. As soon as I found out about FBAR and FATCA I contacted a lawyer I found online, gave him my past UK account sums and he says that it will cost $28,000 or I will be liable for huge fines. It's very scary. I'm not sure where to start with this. He says he has to write a 25 page reasonable cause statement because the legal standard is so high. I received a legacy from my deceased parents too.

Does anyone have any advice where I should start with this? Which form should I look at first? Can my normal US tax preparer do this for me? I am currently out of the States and won't return til August and this is ruining my trip.

Thank you.

Does anyone have any advice where I should start with this? Which form should I look at first? Can my normal US tax preparer do this for me? I am currently out of the States and won't return til August and this is ruining my trip.

Thank you.

Jul 2nd 2025 | 11:26 am

#4

Forum Regular

Joined: Oct 2021

Posts: 76

Yours & actually the folks who I paid to file my tax returns should have informed you/me about FBAR’s, it’s part of their job! Your lawyer is doing what a lot of lawyers try to do, prey on regular folks who are intimidated by legal matters & trying to extract money from you for services which you can do yourself. Please don’t worry about this too much, Google FBAR & follow the instructions. If you have assets or bank accounts over $10,000 going back a number of years in the UK then report them to the IRS. It really isn’t a big deal, it just seems to be.

Jul 2nd 2025 | 11:42 am

#5

Furby

Joined: Apr 2016

Posts: 1,188

From: St. Louis, MO.

Unfortunately, the IRS can (and do) apply the very stiff statutory penalties for failure to report these accounts. Fortunately there are options to avoid these penalties. If US tax was paid on the foreign accounts then it is easy to fix yourself or to use a domestic CPA to do so at very reasonable cost. If US tax was not paid on the income then it involves more cost and/or risk. The IRS is very reasonable if all overseas income was declared on your US tax return and US tax paid, less so if there is unreported income and delinquent taxes.

The threshold for filing an FBAR is an aggregate balance in foreign accounts greater than $10K. The threshold for Form 8938 to be attached to your tax return is an aggregate balance in foreign accounts that exceeds $75K/$150K at any time throughout the tax year or $50K/$100K at the end of the tax year (single/married). Foreign accounts are everything held overseas including bank accounts, bonds, investment accounts, ISAs, life insurance and any pension with a known cash value. Basically everything except property and collectibles.

If you declared all income from any overseas accounts and paid US tax on that income, or there was no income from those accounts, then you should file the prior 6 years FBARS and amend the prior 3 years tax returns to include Form 8938 with a statement of reasonable cause. That is fairly easy to do yourself at no cost if you are detail oriented. Otherwise a decent accountant should be able to do it for you at a very reasonable cost, likely in the range of a few thousand, probably a lot less. The IRS will not apply fines and penalties so long as all overseas income was declared and tax paid. They will not necessarily select those returns for audit but could do so in which case you have no further concerns unless there is anything of interest on the audited returns (beyond the unreported accounts).

If you did not pay US tax on any foreign income (however small that may be) then you can still follow the same process as above (but paying the delinquent tax) however in these circumstances the IRS can apply the stiff statutory penalties and fines without being required to consider mitigating circumstances (what they call reasonable cause). The benefits are that the amended tax returns and late FBARs could (likely will) be accepted with no penalties or fines applied but the risk is that if you are unlucky and are audited you could have the book thrown at you which would be substantially worse than the other option which is to use the streamlined domestic offshore procedure which applies a 5% penalty to the highest aggregate balance of the unreported accounts. The 5% penalty is the cost of the guarantee to avoid the much serious statutory penalties.

If you used a professional to file your taxes and have proof that you informed them of your foreign accounts then you should go back to them and ask them to fix this at their cost. Otherwise your options are as above. If you did pay taxes on the overseas income then I would either do it myself as described above or approach a domestic CPA. If you did not pay taxes on any overseas income then you probably do want to use a professional familiar with this scenario. There are some out there who will perform this service for a much more reasonable fee than $28K. For that fee to apply there would need to be very large balances involved or they are simply a shark. Either way you need to shop around.

Detailed information of each of the above options is available here if you drill down into the links. https://www.irs.gov/individuals/inte...ion-procedures

The threshold for filing an FBAR is an aggregate balance in foreign accounts greater than $10K. The threshold for Form 8938 to be attached to your tax return is an aggregate balance in foreign accounts that exceeds $75K/$150K at any time throughout the tax year or $50K/$100K at the end of the tax year (single/married). Foreign accounts are everything held overseas including bank accounts, bonds, investment accounts, ISAs, life insurance and any pension with a known cash value. Basically everything except property and collectibles.

If you declared all income from any overseas accounts and paid US tax on that income, or there was no income from those accounts, then you should file the prior 6 years FBARS and amend the prior 3 years tax returns to include Form 8938 with a statement of reasonable cause. That is fairly easy to do yourself at no cost if you are detail oriented. Otherwise a decent accountant should be able to do it for you at a very reasonable cost, likely in the range of a few thousand, probably a lot less. The IRS will not apply fines and penalties so long as all overseas income was declared and tax paid. They will not necessarily select those returns for audit but could do so in which case you have no further concerns unless there is anything of interest on the audited returns (beyond the unreported accounts).

If you did not pay US tax on any foreign income (however small that may be) then you can still follow the same process as above (but paying the delinquent tax) however in these circumstances the IRS can apply the stiff statutory penalties and fines without being required to consider mitigating circumstances (what they call reasonable cause). The benefits are that the amended tax returns and late FBARs could (likely will) be accepted with no penalties or fines applied but the risk is that if you are unlucky and are audited you could have the book thrown at you which would be substantially worse than the other option which is to use the streamlined domestic offshore procedure which applies a 5% penalty to the highest aggregate balance of the unreported accounts. The 5% penalty is the cost of the guarantee to avoid the much serious statutory penalties.

If you used a professional to file your taxes and have proof that you informed them of your foreign accounts then you should go back to them and ask them to fix this at their cost. Otherwise your options are as above. If you did pay taxes on the overseas income then I would either do it myself as described above or approach a domestic CPA. If you did not pay taxes on any overseas income then you probably do want to use a professional familiar with this scenario. There are some out there who will perform this service for a much more reasonable fee than $28K. For that fee to apply there would need to be very large balances involved or they are simply a shark. Either way you need to shop around.

Detailed information of each of the above options is available here if you drill down into the links. https://www.irs.gov/individuals/inte...ion-procedures

Last edited by Glasgow Girl; Jul 2nd 2025 at 11:52 am.

Jul 2nd 2025 | 12:33 pm

#6

Thread Starter

Forum Regular

Joined: Jun 2020

Posts: 96

Unfortunately, the IRS can (and do) apply the very stiff statutory penalties for failure to report these accounts. Fortunately there are options to avoid these penalties. If US tax was paid on the foreign accounts then it is easy to fix yourself or to use a domestic CPA to do so at very reasonable cost. If US tax was not paid on the income then it involves more cost and/or risk. The IRS is very reasonable if all overseas income was declared on your US tax return and US tax paid, less so if there is unreported income and delinquent taxes.

The threshold for filing an FBAR is an aggregate balance in foreign accounts greater than $10K. The threshold for Form 8938 to be attached to your tax return is an aggregate balance in foreign accounts that exceeds $75K/$150K at any time throughout the tax year or $50K/$100K at the end of the tax year (single/married). Foreign accounts are everything held overseas including bank accounts, bonds, investment accounts, ISAs, life insurance and any pension with a known cash value. Basically everything except property and collectibles.

If you declared all income from any overseas accounts and paid US tax on that income, or there was no income from those accounts, then you should file the prior 6 years FBARS and amend the prior 3 years tax returns to include Form 8938 with a statement of reasonable cause. That is fairly easy to do yourself at no cost if you are detail oriented. Otherwise a decent accountant should be able to do it for you at a very reasonable cost, likely in the range of a few thousand, probably a lot less. The IRS will not apply fines and penalties so long as all overseas income was declared and tax paid. They will not necessarily select those returns for audit but could do so in which case you have no further concerns unless there is anything of interest on the audited returns (beyond the unreported accounts).

If you did not pay US tax on any foreign income (however small that may be) then you can still follow the same process as above (but paying the delinquent tax) however in these circumstances the IRS can apply the stiff statutory penalties and fines without being required to consider mitigating circumstances (what they call reasonable cause). The benefits are that the amended tax returns and late FBARs could (likely will) be accepted with no penalties or fines applied but the risk is that if you are unlucky and are audited you could have the book thrown at you which would be substantially worse than the other option which is to use the streamlined domestic offshore procedure which applies a 5% penalty to the highest aggregate balance of the unreported accounts. The 5% penalty is the cost of the guarantee to avoid the much serious statutory penalties.

If you used a professional to file your taxes and have proof that you informed them of your foreign accounts then you should go back to them and ask them to fix this at their cost. Otherwise your options are as above. If you did pay taxes on the overseas income then I would either do it myself as described above or approach a domestic CPA. If you did not pay taxes on any overseas income then you probably do want to use a professional familiar with this scenario. There are some out there who will perform this service for a much more reasonable fee than $28K. For that fee to apply there would need to be very large balances involved or they are simply a shark. Either way you need to shop around.

Detailed information of each of the above options is available here if you drill down into the links. https://www.irs.gov/individuals/inte...ion-procedures

The threshold for filing an FBAR is an aggregate balance in foreign accounts greater than $10K. The threshold for Form 8938 to be attached to your tax return is an aggregate balance in foreign accounts that exceeds $75K/$150K at any time throughout the tax year or $50K/$100K at the end of the tax year (single/married). Foreign accounts are everything held overseas including bank accounts, bonds, investment accounts, ISAs, life insurance and any pension with a known cash value. Basically everything except property and collectibles.

If you declared all income from any overseas accounts and paid US tax on that income, or there was no income from those accounts, then you should file the prior 6 years FBARS and amend the prior 3 years tax returns to include Form 8938 with a statement of reasonable cause. That is fairly easy to do yourself at no cost if you are detail oriented. Otherwise a decent accountant should be able to do it for you at a very reasonable cost, likely in the range of a few thousand, probably a lot less. The IRS will not apply fines and penalties so long as all overseas income was declared and tax paid. They will not necessarily select those returns for audit but could do so in which case you have no further concerns unless there is anything of interest on the audited returns (beyond the unreported accounts).

If you did not pay US tax on any foreign income (however small that may be) then you can still follow the same process as above (but paying the delinquent tax) however in these circumstances the IRS can apply the stiff statutory penalties and fines without being required to consider mitigating circumstances (what they call reasonable cause). The benefits are that the amended tax returns and late FBARs could (likely will) be accepted with no penalties or fines applied but the risk is that if you are unlucky and are audited you could have the book thrown at you which would be substantially worse than the other option which is to use the streamlined domestic offshore procedure which applies a 5% penalty to the highest aggregate balance of the unreported accounts. The 5% penalty is the cost of the guarantee to avoid the much serious statutory penalties.

If you used a professional to file your taxes and have proof that you informed them of your foreign accounts then you should go back to them and ask them to fix this at their cost. Otherwise your options are as above. If you did pay taxes on the overseas income then I would either do it myself as described above or approach a domestic CPA. If you did not pay taxes on any overseas income then you probably do want to use a professional familiar with this scenario. There are some out there who will perform this service for a much more reasonable fee than $28K. For that fee to apply there would need to be very large balances involved or they are simply a shark. Either way you need to shop around.

Detailed information of each of the above options is available here if you drill down into the links. https://www.irs.gov/individuals/inte...ion-procedures

What constitutes "income?"

On the one hand, you have to report assets over $10k but assets (or savings) aren't income, right? So income would be things like unearned interest on an account, I assume.

And I had a legacy several years ago but a quick google search suggests that a foreign legacy is not taxable in the USA and therefore does not count as income for US tax purpose yet the big time law company I contacted made a deal of the legacy. So would a legacy be subject to tax? Would SDO 5% penalties or other penalties apply to total savings/assets rather than income? What if you had undeclared savings, legacy, but zero or negligible income?

Thanks in advance--you are 10 x more helpful that the lawyer.

Ed

Jul 2nd 2025 | 1:35 pm

#7

Furby

Joined: Apr 2016

Posts: 1,188

From: St. Louis, MO.

Income is any money payed to you other than return of the original investment. For example interest on a bank account, dividends or capital gains on investments or bonds. Or, it could be income paid from a pension plan. There are other types of income but this should provide a good idea of what it could be.

Reporting foreign accounts on an FBAR and Form 8938 is different from reporting income on your 1040. The account details only are reported on an FBAR and Form 8938 but not the actual income. The income is reported on the 1040 but not the accounts themselves. FBAR and Form 8938 are for reporting purposes only, the income reported on the 1040 is to calculate US tax due. It does not matter if tax was paid in a foreign country, all foreign income must be declared on the 1040, and US tax paid. If you did pay foreign tax in a foreign country as well, there are processes to ensure that you are not taxed twice by both countries but that is another subject. The important thing here is that all foreign income is reported (and tax paid) on the US tax return.

A foreign inheritance is not taxed to a US recipient, but if it exceeds $100K then Form 3520 must be filed. This is for reporting purposes only, no tax is due. I don’t think there is any statute of limitations on Form 3520, therefore this form should be filed regardless of how long ago you received these funds because there are stiff fines if the IRS detects that the form is delinquent. After just a few years the chances of that are small unless they are looking at your foreign accounts for other reasons which increases your risk somewhat. The good news is that a reasonable cause statement should be sufficient in this case to avoid any penalty. A good domestic CPA will be able to handle this at reasonable cost. I would use a CPA for this, Form 3520 can be tricky to complete and you really want it to be right, particularly when submitting retrospectively.

The 5% SDOP penalty is calculated from the aggregate balance of all unreported accounts, it is not based upon income. If there was zero foreign income from all accounts then the no cost/no penalty processes can be utilized with no risk. If there was any unreported foreign income on any account, no matter how little (even $1), then utilizing the no cost/no penalty processes runs the risk of having statutory fines and penalties applied to all unreported accounts.

If you only have a small amount of unreported income, I would scrutinize your prior 3 years tax returns to determine if you can find any way in which you may have missed out an a deduction or can otherwise reduce your tax bill for those years enough that there is no unpaid tax when the foreign income is included. If you paid tax on that income in a foreign country that may provide a US tax credit that makes it such that no additional US tax is due. A CPA may find other options to reduce prior year taxes. Any of that could be a get out jail free card.

All things considered, I think you should approach a good domestic CPA, not a generic big box outfit like H&R Block. They should be able to take care of you at reasonable cost. I wouldn’t worry too much. Worst case you can get out of this mess with a 5% penalty and few thousand dollars in fees, best case no penalty and some very reasonable fees. Hundreds of people have been in your position and navigated it successfully.

Reporting foreign accounts on an FBAR and Form 8938 is different from reporting income on your 1040. The account details only are reported on an FBAR and Form 8938 but not the actual income. The income is reported on the 1040 but not the accounts themselves. FBAR and Form 8938 are for reporting purposes only, the income reported on the 1040 is to calculate US tax due. It does not matter if tax was paid in a foreign country, all foreign income must be declared on the 1040, and US tax paid. If you did pay foreign tax in a foreign country as well, there are processes to ensure that you are not taxed twice by both countries but that is another subject. The important thing here is that all foreign income is reported (and tax paid) on the US tax return.

A foreign inheritance is not taxed to a US recipient, but if it exceeds $100K then Form 3520 must be filed. This is for reporting purposes only, no tax is due. I don’t think there is any statute of limitations on Form 3520, therefore this form should be filed regardless of how long ago you received these funds because there are stiff fines if the IRS detects that the form is delinquent. After just a few years the chances of that are small unless they are looking at your foreign accounts for other reasons which increases your risk somewhat. The good news is that a reasonable cause statement should be sufficient in this case to avoid any penalty. A good domestic CPA will be able to handle this at reasonable cost. I would use a CPA for this, Form 3520 can be tricky to complete and you really want it to be right, particularly when submitting retrospectively.

The 5% SDOP penalty is calculated from the aggregate balance of all unreported accounts, it is not based upon income. If there was zero foreign income from all accounts then the no cost/no penalty processes can be utilized with no risk. If there was any unreported foreign income on any account, no matter how little (even $1), then utilizing the no cost/no penalty processes runs the risk of having statutory fines and penalties applied to all unreported accounts.

If you only have a small amount of unreported income, I would scrutinize your prior 3 years tax returns to determine if you can find any way in which you may have missed out an a deduction or can otherwise reduce your tax bill for those years enough that there is no unpaid tax when the foreign income is included. If you paid tax on that income in a foreign country that may provide a US tax credit that makes it such that no additional US tax is due. A CPA may find other options to reduce prior year taxes. Any of that could be a get out jail free card.

All things considered, I think you should approach a good domestic CPA, not a generic big box outfit like H&R Block. They should be able to take care of you at reasonable cost. I wouldn’t worry too much. Worst case you can get out of this mess with a 5% penalty and few thousand dollars in fees, best case no penalty and some very reasonable fees. Hundreds of people have been in your position and navigated it successfully.

Last edited by Glasgow Girl; Jul 2nd 2025 at 1:58 pm.

Jul 2nd 2025 | 11:27 pm

#8

Forum Regular

Joined: Feb 2024

Posts: 151

From: Scotland

You can absolutely do the FBARs yourself - time consuming to go back and track down data but completely do-able (I went back and filed 5 missed years this year, gave the reason for late submission that "I did not know that I had to file", and everything was accepted.) As Glasgow Girl says, a decent CPA should be able to help with the IRS side, you don't need to pay lawyers' hourly rates for this.

Jul 2nd 2025 | 11:31 pm

#9

Thread Starter

Forum Regular

Joined: Jun 2020

Posts: 96

Thank you all. I owe you an immense debt. I might have some follow ups if that is okay, but I am working through all of this now, slowly, familiarizing myself with all the details before I find a CPA to work with (which is hard when you have no contacts). At least I am calmer now.

Ed.

Ed.

Jul 2nd 2025 | 11:54 pm

#10

Furby

Joined: Apr 2016

Posts: 1,188

From: St. Louis, MO.

Google CPAs. Call a few and ask if they have any experience in filing FBARS and Form 8938 (if that is applicable). In a reasonable sized city there should be plenty with this experience. Even in rural areas there should be someone familiar with this process. You want someone with experience because they will be up to date with the latest options, be able to accurately assess your risk if using the no cost/no fee process, and cost less because they already have the knowledge and don’t need to do a lot of research. Many will accept remote clients so you don’t necessarily need to be close by. Filing yourself is an option but with undeclared income and unpaid tax, you likely will be best guided by a professional, plus you may have Form 3520 to file if the inheritance was greater than $100K. Avoid the ones that advertise heavily as an FBAR and/or FATCA attorney. Although there are a few good ones out there, many will scare you to death unnecessarily and rob you blind.

Jul 3rd 2025 | 12:13 am

#11

SUPER MODERATOR

Joined: Dec 2005

Posts: 89,087

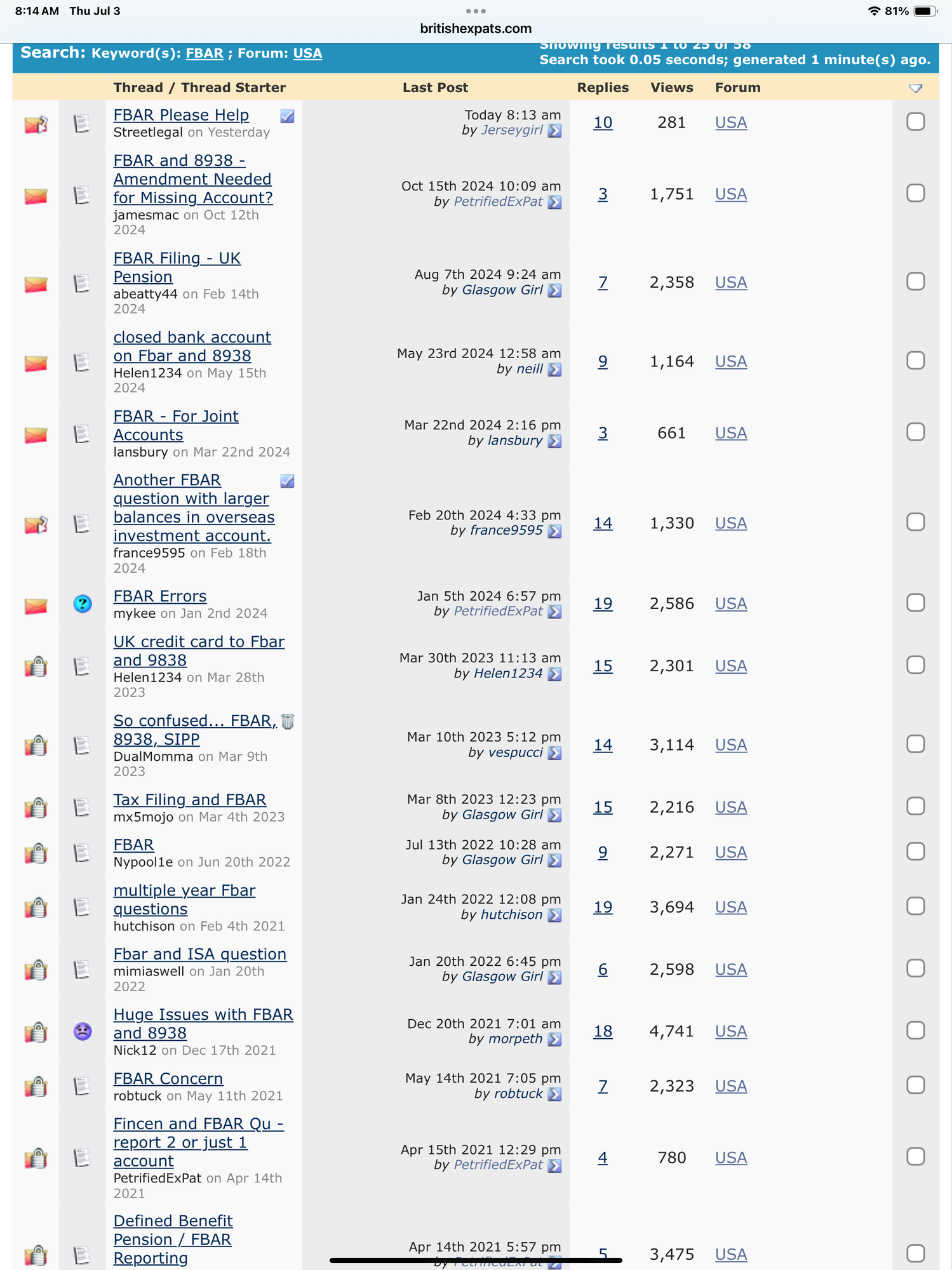

A search of the US forum will bring up threads discussing this subject. Below is a link to the search, but it will probably expire after a while.

https://britishexpats.com/forum/sear...rchid=15320922

Also a screen shot of the page.

https://britishexpats.com/forum/sear...rchid=15320922

Also a screen shot of the page.

Jul 3rd 2025 | 1:41 am

#13

Furby

Joined: Apr 2016

Posts: 1,188

From: St. Louis, MO.

For Form 3520 and Form 8938, the IRS has three years after the form is filed to assess any penalties or fines, but it is open ended until the form is filed. The FBAR statute of limitations is 6 years from the original deadline for filing for any particular year.

In the case of Form 3520 reporting an inheritance a simple reasonable cause statement such as you were not aware of the need to file should eliminate any risk of fines and penalties arising from that form. In the case of FBARs and Form 8938 the risk is minimal if all income was declared, tax paid, and the proper process followed. If there is undeclared foreign income and unpaid US tax on that income then the risk of statutory fines and penalties increase unless the SDOP procedures are used with the associated 5% penalty.

In the case of Form 3520 reporting an inheritance a simple reasonable cause statement such as you were not aware of the need to file should eliminate any risk of fines and penalties arising from that form. In the case of FBARs and Form 8938 the risk is minimal if all income was declared, tax paid, and the proper process followed. If there is undeclared foreign income and unpaid US tax on that income then the risk of statutory fines and penalties increase unless the SDOP procedures are used with the associated 5% penalty.

Jul 3rd 2025 | 2:36 am

#14

Thread Starter

Forum Regular

Joined: Jun 2020

Posts: 96

Again, thank you. I'll find a CPA but just so I proceed with knowledge, I would be grateful for some clarifications (forgive the lack of financial acumen):I will find a CPA—I have read each post and downloaded the forms (yet to read) and I have a few clarification questions if that is okay:

1. I may have misunderstood the statute of limitations given advice above; to clarify—will I need to submit 1040 for the past 3 years & FBAR for 6 years or each for as long as I have been a permanent resident?

2. Given that foreign income should have been declared on each 1040, a CPA will need access to previous 1040 submissions (is this just for the past 3 tax years?) and any foreign income will complicate the overall tax submission (eg., potentially changing tax brackets)? Seems potentially quite tricky for me as I use a tax preparer.

3. Does one submit three years of individual 8939s etc or do retrospective tax submissions go on one form?

4. How is the SDO calculated—is it 5% on assets for each year (for three years?) and then added together for a total sum? Or it it "one-off"?

5. To calculate assets do you use the end of tax year (31/12) for each submission?

6. Is the “reasonable cause†a separate form? Is it submitted separately for FBAR and for IRS?

7. Does one attach copies of their UK assets (eg., bank statements) or just fill in the appropriate numbers?

1. I may have misunderstood the statute of limitations given advice above; to clarify—will I need to submit 1040 for the past 3 years & FBAR for 6 years or each for as long as I have been a permanent resident?

2. Given that foreign income should have been declared on each 1040, a CPA will need access to previous 1040 submissions (is this just for the past 3 tax years?) and any foreign income will complicate the overall tax submission (eg., potentially changing tax brackets)? Seems potentially quite tricky for me as I use a tax preparer.

3. Does one submit three years of individual 8939s etc or do retrospective tax submissions go on one form?

4. How is the SDO calculated—is it 5% on assets for each year (for three years?) and then added together for a total sum? Or it it "one-off"?

5. To calculate assets do you use the end of tax year (31/12) for each submission?

6. Is the “reasonable cause†a separate form? Is it submitted separately for FBAR and for IRS?

7. Does one attach copies of their UK assets (eg., bank statements) or just fill in the appropriate numbers?

Jul 3rd 2025 | 3:49 am

#15

Joined: Dec 2001

Posts: 53,356

From: Dixie, ex UK

That, and straight-up tax fraud, by people with $millions in accounts outside the US, and especially in historically secretive* off-shore financial centres, like Switzerland, the Cayman Islands, the Channel Islands, and Cyprus, among others.

* Most off-shore banking centres have now reached agreements with the US, UK, and EU countries to report accounts to each country's taxing authority.

* Most off-shore banking centres have now reached agreements with the US, UK, and EU countries to report accounts to each country's taxing authority.